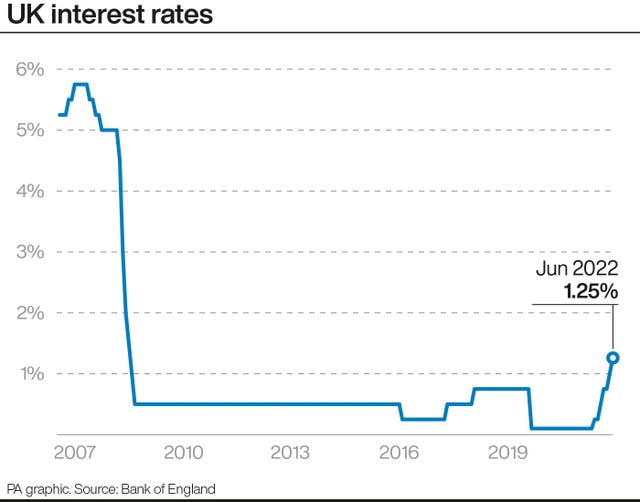

The Bank of England has raised its interest base rate to the highest point since the start of 2009 as it hiked its inflation predictions for the autumn.

The Bank’s experts set the rate at 1.25%, a rise from 1% previously, and the fifth increase in a row as it tries to tame runaway inflation.

It also warned that prices for households across the country might increase even further than previously thought.

Three of the nine-person Monetary Policy Committee (MPC) voted for an even bigger hike, arguing that rates should rise as high as 1.5%.

“In view of continuing signs of robust cost and price pressures, including the current tightness of the labour market, and the risk that those pressures become more persistent, the committee voted to increase Bank rate by 0.25 percentage points,” it said in a notice.

For the MPC, which decides on rates, a key concern is inflation.

The committee is tasked with keeping inflation constant at around 2%, a target it is currently well clear of.

The cost of living has been soaring for months, with consumer prices index (CPI) inflation hitting a 40-year high of 9% in April when the energy price cap was hiked.

But things are set to get even worse later this year.

Experts currently expect that regulator Ofgem could put up energy prices even further, from £1,971 per year to around £2,800.

This, alongside other pressures in the economy, could lead to CPI topping 11% in October, the Bank said.

Just a month ago it had predicted inflation to peak at above 10%.

“The economy has recently been subject to a succession of very large shocks,” Bank governor Andrew Bailey wrote in a letter to Chancellor Rishi Sunak setting out why inflation was so much higher than the 2% target.

“These shocks have pushed global energy and tradable goods prices to elevated levels.

“Those price increases have raised UK inflation and, since the United Kingdom is a net importer of these items, will necessarily weigh on most UK households’ real incomes and many UK companies’ real profits.”

The Chancellor has announced multi-billion pound help for struggling households, much of which is set to come in when energy bills rise again in October.

But it might prove somewhat of a double-edged sword, the Bank said, adding another 0.1 percentage points to CPI in the first year.

In its reports on Thursday the Bank also downgraded its forecast for gross domestic product (GDP) for the second quarter of the year.

GDP is now expected to drop by 0.3% across the quarter, weaker than anticipated just over a month ago.

The Bank’s base rate has been low since being cut rapidly during the financial crisis. It has risen recently in response to what is happening in the economy.

It is the only time since records began in 1694 that the base rate has been set at 1.25%. In February 2009, the rate was lowered from 1.5% to 1%, skipping the step in between.

Labour shadow chief secretary to the Treasury, Pat McFadden, said: “Many families will be worrying about the impact this will have on their household bills.

“We need a plan for a stronger, more stable economy, that can weather the short-term issues and fix the foundations for the long term.”

British Chambers of Commerce head of research, David Bharier, added: “While expected, the decision to raise the interest rate will add further concern to businesses amid a weakened economic outlook, soaring cost pressures, and labour shortages.

“The increase signals the Bank’s intention to tackle inflation but businesses have been raising the alarm about spiralling prices since the start of 2021 and a higher interest rate is unlikely to address many of the global causes of this.”

Comments: Our rules

We want our comments to be a lively and valuable part of our community - a place where readers can debate and engage with the most important local issues. The ability to comment on our stories is a privilege, not a right, however, and that privilege may be withdrawn if it is abused or misused.

Please report any comments that break our rules.

Read the rules here